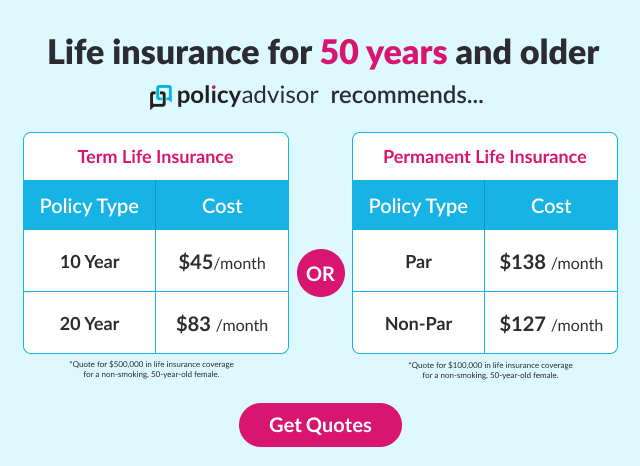

Finding a life insurance policy with $500,000 coverage for as little as $1 per month is certainly appealing, especially for those on a tight budget who want to secure their loved ones’ financial future. While such rates can exist, they are often dependent on a very specific set of circumstances. This article will delve into the factors that make such affordable coverage possible, who is most likely to qualify, and what to consider when seeking these low-cost options.

Introduction: Affordable Security – The Promise of Low-Cost Life Insurance

Life insurance is a fundamental component of financial planning, designed to provide a financial safety net for your loved ones in the event of your untimely demise. It ensures that your dependents can maintain their lifestyle, cover essential expenses, pay off debts, and achieve future goals even if you’re no longer there to provide for them. For many, the perceived high cost of life insurance can be a deterrent, leading them to postpone or forgo this crucial protection.

However, the landscape of life insurance has evolved, with options emerging that are surprisingly affordable. Specifically, securing a $500,000 life insurance policy for around $10 per month is a possibility, primarily through term life insurance. This article will explore the realistic pathways to obtaining such coverage, the key factors that influence premiums, and important considerations to help you find an affordable policy that offers peace of mind without breaking the bank.

The Quest for $500K Coverage at $1/Month: Understanding the Realities

While the idea of a $500,000 life insurance policy for $10 a month sounds incredibly attractive, it’s essential to understand the underlying factors that make such a low premium possible. These rates are typically achievable for a very specific demographic and policy type.

The Power of Term Life Insurance

The primary reason you might find such affordable rates is the type of policy: term life insurance.

- Pure Protection: Term life insurance is straightforward. It provides coverage for a specific period (the “term”), such as 10, 20, or 30 years. If the insured passes away within this term, the beneficiaries receive the death benefit. If the term expires and the insured is still alive, the policy simply ends, and there’s no payout.

- No Cash Value: Unlike permanent life insurance policies (like whole life or universal life) which build cash value over time, term life insurance does not. This lack of a savings or investment component makes term life significantly more affordable, as premiums are solely for mortality risk coverage.

- Affordability: Because term life policies only provide coverage for a defined period and do not accumulate cash value, they are the most budget-friendly option for securing a substantial death benefit. This is why a $100,000 cover for $10/month is generally a term life offering.

Who Qualifies for Such Low Rates? The Ideal Candidate Profile

The $10/month for $500,000 coverage is typically reserved for individuals who pose the lowest risk to the insurer. This “ideal candidate” usually fits the following profile:

1. Young Age is Key

Age is the most significant determinant of life insurance premiums. The younger you are when you purchase a policy, the lower your premiums will be.

- Lower Mortality Risk: Insurance companies calculate premiums based on mortality rates. Younger individuals have a statistically lower risk of dying within the policy term.

- Typical Age Bracket: You are most likely to qualify for a $10/month premium for $100,000 coverage if you are in your 20s or early 30s. As you age, even by a few years, the premium can increase significantly. For example, a 40-year-old might pay $15-$25/month for the same coverage, and a 50-year-old even more.

2. Excellent Health is Paramount

Your health status plays a crucial role in underwriting. Insurers conduct a risk assessment, and pristine health translates to lower premiums.

- No Pre-existing Conditions: This means no history of chronic illnesses like diabetes, hypertension, heart disease, or cancer.

- Healthy BMI: Being within a healthy weight range is important.

- Normal Medical Exam Results: Many policies, especially for competitive rates, require a medical exam (blood test, urine test, blood pressure, etc.). Favorable results are essential. Policies advertised as “no medical exam” might be more expensive.

3. Non-Smoker Status is Essential

Smoking is a major risk factor for many diseases and significantly shortens life expectancy. Insurers heavily penalize smokers.

- Higher Premiums for Smokers: A smoker could pay two to three times more than a non-smoker for the same coverage. If you’ve quit, you often need to be smoke-free for several years (typically 2-5 years) to qualify for non-smoker rates.

- Tobacco Use Definition: Be aware that “tobacco use” often includes cigarettes, cigars, chewing tobacco, e-cigarettes, and vaping.

4. Favorable Family Medical History

While you can’t control your genetics, insurers do look at your family’s medical history, particularly for immediate family members (parents, siblings).

- Hereditary Conditions: A family history of certain critical illnesses (e.g., early-onset heart disease or cancer) can increase your perceived risk and, consequently, your premiums, even if you are currently healthy.

Clean Lifestyle and Occupation

Your lifestyle and profession also factor into the premium calculation.

- No Risky Hobbies: Engaging in hazardous hobbies like skydiving, scuba diving, rock climbing, or car racing can lead to higher premiums.

- Non-Hazardous Occupation: Occupations with inherent risks (e.g., pilots, construction workers, miners, military personnel) generally face higher premiums. A desk job or other low-risk profession is ideal for securing the lowest rates.

- Good Driving Record: A history of multiple traffic violations or DUIs can also negatively impact your rates as it indicates a higher risk.

The Role of the Term Length

The length of the term also influences the premium. A shorter term (e.g., 5 or 10 years) will generally have lower monthly premiums than a longer term (e.g., 20 or 30 years) for the same sum assured. If you are seeing rates as low as $10/month for $500,000, it’s likely for a shorter term (e.g., 10-15 years) for a young, healthy individual.

Finding Your $1/Month Policy: Practical Steps

Even if you fit the “ideal candidate” profile, finding the exact $10/month policy requires diligent research and comparison.

Shop Around and Compare Quotes

Do not settle for the first quote you receive. Life insurance premiums can vary significantly between providers for the same coverage amount due to differing underwriting guidelines and risk assessment models.

- Online Aggregators: Use online insurance comparison websites to get multiple quotes simultaneously.

- Direct from Insurers: Visit the websites of reputable insurance companies directly to get quotes.

- Independent Agents: Work with an independent insurance agent who can shop around with various carriers on your behalf and help you compare options.

2. Be Honest on Your Application

It is crucial to provide accurate and truthful information on your application. Misrepresenting your health, lifestyle, or family history can lead to serious consequences.

- Policy Invalidation: If an insurer discovers you provided false information, they can deny the claim, leaving your beneficiaries without the financial support you intended.

- Higher Future Premiums: Even if the policy isn’t immediately invalidated, future policies might become more expensive if your misrepresentation is discovered.

3. Consider Limited Pay Options (for a different perspective)

While not directly related to the monthly $10 premium, some term plans offer “limited pay” options where you pay premiums for a shorter period (e.g., 5 or 10 years) but remain covered for a longer term. While the monthly payments during the payment period would be higher than $10, the total premium paid over the life of the policy might be less, offering long-term savings. This is a different approach to affordability.

4. Don’t Overlook Reputable Insurers

While looking for the cheapest option, ensure the insurance company has a strong financial rating and a good claim settlement ratio. A low premium is irrelevant if the company struggles to pay out claims. In India, look for the Claim Settlement Ratio (CSR) published by IRDAI. A higher CSR indicates a better track record.

Is $500,000 Enough Coverage? A Crucial Consideration

While a $100,000 policy for $10/month is a great start for affordability, it’s essential to assess whether $100,000 in coverage is actually sufficient for your family’s needs.

- Debt Repayment: Does it cover outstanding debts like mortgages, car loans, or personal loans?

- Income Replacement: How many years of your income would $500,000 replace? (e.g., if you earn $20,000 annually, it’s only 20 years of income).

- Future Expenses: Does it account for future expenses like children’s education, marriage, or other long-term financial goals?

- Inflation: Consider that $500,000 today will have less purchasing power in 10 or 20 years due to inflation.

For many individuals, especially those with dependents, $500,000 might be a starting point but may not be enough to fully secure their family’s financial future. It’s crucial to balance affordability with adequate coverage. You might consider buying a smaller policy now at a low cost and increasing your coverage later as your income grows and needs change, or opt for a slightly higher premium for a larger sum assured if your budget allows.

Summary: The Path to Affordable Life Protection

Securing a $500,000 life insurance policy for around $1 per month is a realistic goal, primarily achievable with term life insurance. This highly affordable option is generally available to:

- Young individuals (20s to early 30s)

- Those in excellent health with no pre-existing conditions

- Non-smokers

- Individuals with a favorable family medical history and low-risk occupations/lifestyles.

- Opting for shorter policy terms (e.g., 10-15 years) can also contribute to lower premiums.

To find such a policy, it’s crucial to:

- Compare quotes from multiple insurers.

- Be completely honest in your application.

- Prioritize insurers with strong financial ratings and high claim settlement ratios.

- Crucially, assess if $500,000 is truly sufficient for your dependents’ long-term financial needs, considering debt, income replacement, and future goals.

Conclusion: Value and Vision in Life Insurance

Life insurance is not a luxury; it’s a fundamental aspect of responsible financial planning that offers invaluable peace of mind. The good news is that securing meaningful coverage doesn’t always have to come with a hefty price tag. For young, healthy non-smokers, a $500,000 term life insurance policy for as little as $10 per month is a tangible reality, providing essential financial protection for your loved ones at an incredibly accessible cost.

While these highly competitive rates target a specific demographic, the principles of securing affordable life insurance remain universal: buy young, maintain good health, and thoroughly compare options from reputable providers. Even if your circumstances mean a slightly higher premium, the cost of not having life insurance far outweighs the investment. Take the proactive step today to explore your options and secure a policy that protects your family’s financial future, allowing them to navigate life’s uncertainties with greater security and confidence. Don’t let perceived cost be a barrier to this vital financial safeguard.